Cities with extremely educated labor forces have an advantage in bring in knowledge-based tasks. On the other hand, purchasing facilities to enhance railway, bridges and roads assists metros afflicted by getting worse traffic and bad connections between submarkets. The consensus amongst economic experts has coalesced around the view that the U.S. can run larger deficits than formerly thought without harming the economy.

Bernard Yaros, a financial expert and assistant director of federal financial policy at Moody's Analytics, says that a research study by his company figured out that the "moment of truth" would come when financial obligation reached 260 percent of GDP. "The takeaway is that over the long term, [debt] is destructive, however high levels of debt isn't an issue until we hit the breaking point where debt spirals out of control and financiers despair in the U.S.

Keith Hall, former director of the Congressional Budget Office and now a teacher at the McCourt School of Public Policy at Georgetown University, says the previous 5 CBO directors and previous 4 chairs of the Federal Reserve have actually called the growth in federal debt unsustainable. He said it is shortsighted to take the mindset that given that nothing bad has happened, absolutely nothing bad will take place in the future.

The 10-Second Trick For Who Took Over Abn Amro Mortgages

It's homebuying season, and patterns indicate the home mortgage market continues to develop. Impressive home loan balances increased for the seventh straight quarter reaching a new high of $9 - what are cpm payments with regards to fixed mortgages rates. 5 trillion, according to Experian data from the first quarter (Q1) of 2019. That figure is well above the exceptional balances reported throughout the peak of the mortgage crisis in 2008.

And for customers just starting their homebuying search, low rates of interest and readily available stock might make their search more rewarding, depending upon local market conditions. The variety of U.S. houses offered for sale stayed flat year over year in Q1 2019the very first time house stock hasn't reduced in 3 years, according to Trulia.

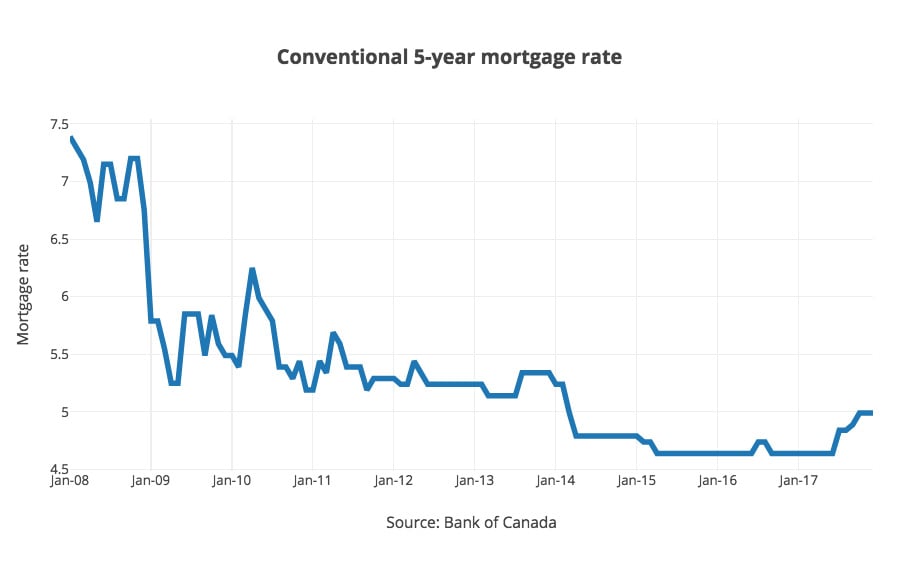

1% from May 2018 to May of this year. Of the houses offered in May 2019, 53% were on the marketplace for less than a month, according to NAR. Meanwhile, interest rates are anticipated to stay listed below 5% in 2019, according to the Home loan Bankers Association (MBA). It anticipates 30-year home loan rates will balance 4.

The Main Principles Of How Many New Mortgages Can I Open

4% through the second half of 2019 (mortgages what will that house cost). While home loan balances climb, delinquency rates have actually progressively decreased for many years. Because 2009, payments made between 30 and 59 days late have decreased 61%. There were decreases throughout the board, with the exception of a little increase this previous year for payments 30 days late.

home loan financial obligation per customer for Q1 2019 was $202,284, a 2. 4% year-over-year boost for 2019. Increasing Visit this page home mortgage financial obligation is no surprise when taking a look at housing expense increases compared with earnings development. The average list prices for brand-new homes increased 46% over the previous ten years, according to U.S. Census Bureau information and Federal Reserve Economic information, while the mean household earnings has actually increased just 3% throughout the exact same time period.

37% Source: Experian, Zillow, Freddie MacSubprime mortgage financial obligation increased 1. 4% in the very first quarter of 2019 with an average balance of $161,408. Citizens of Washington, D.C., carried the highest average mortgage debt for the second year in a row, at $416,848 per borrower. California ranked 2nd, followed by Hawaii, Washington state and Colorado.

Which Australian Banks Lend To Expats For Mortgages for Dummies

Indiana, Mississippi, Ohio and Kentucky rounded out the 5 states with the least expensive home loan financial obligation. Home mortgage financial obligation in Louisiana rose more than any other state year over year, with a 4% increase in Q1 2019. Next in line with greatest increases were Have a peek at this website Texas, Utah, Colorado, Idaho and Massachusetts. In reality, every state saw an increase to its average home loan debt except Connecticut and New Mexico, whose typical balance reduced by less than 1%.

San Jose-Sunnyvale-Santa Clara, California, had the greatest typical home mortgage debt, at $519,576. Completing the top 5 markets with the most mortgage debt were San Francisco-Oakland-Fremont, California; Santa Barbara-Santa Maria-Goleta, California; Los Angeles-Long Beach-Santa Ana, California; and Santa Cruz-Watsonville, California. House owners in Danville, Illinois, owed the least on their homes, with an average of $70,964 in home loan debt in Q1 2019.

When looking at mortgage financial obligation modifications by city area, Texas held four of the top 5 markets with the greatest increases in the previous year. The leading area went to Bowling Green, Kentucky, however, as its home mortgage financial obligation increased 8. 4%. The next 4 spots, all in Texas, were Sherman-Denison, with an 8.

The Ultimate Guide To What Law Requires Hecm Counseling For Reverse Mortgages

4% boost; Midland, at 6. 9%; and Brownsville-Harlingen, with an increase of 6. 4%. Keep in mind: Data is from Q1 of each yearSource: ExperianYour home loan financial obligation appears on your credit report and is one of lots of elements that can influence your credit history. The majority of credit report think about the total quantity of financial obligation you have, your credit mix (types of debt), queries for brand-new credit, and your payment history.

If you're ready to take on a home loan, inspect out our resources on what to do to prepare for purchasing a home and find out more about good credit scores. While there are no set minimum credit rating to buy a home, having greater credit history will increase the possibility you'll be authorized for a mortgage and conserve cash on lower rates of interest.

If you're thinking about taking out a mortgage, you require to understand the rules regarding your DTI-- that's your debt-to-income ratio for home mortgage loans. That's because your debt-to-income ratio is one of the key elements that identifies loan approval. The consider a variety of criteria when choosing whether to approve you for a home mortgage.

9 Simple Techniques For What Law Requires Hecm Counseling For Reverse Mortgages

Mortgage business need to know you're not getting in over your head financially. If your debt-to-income ratio is too high, you may be denied a home loan. Even if you're accepted, you might need to pay a greater interest rate on your home loan. A debt-to-income ratio for mortgage loans is a basic ratio measuring how much of your earnings goes towards making payments on debt.

Home mortgage loan providers red weeks timeshare utilize your pre-tax, or gross earnings, when calculating your debt-to-income ratio for mortgage approval. Your home loan lending institution will likewise consider only the minimum required payments on your financial obligation, even if you select to pay more than the minimum. For instance, let's state your gross regular monthly earnings is $5,000 a month and these are your debts: A $250 monthly payment for your carA $50 minimum monthly payment on your charge card debtA $125 monthly personal loan payment$ 800 in month-to-month real estate costsYour total regular monthly financial obligation payments including your charge card payment, car loan, home loan payment, and individual loan payment would be $1,225.

5%. Many home loan loan providers consider 2 various debt-to-income ratios when they're deciding whether to offer you a mortgage loan and how much to provide. The two ratios include: The front-end ratio: The front-end ratio is the quantity of your month-to-month earnings that will go to housing expenses after you've purchased your house.

A Biased View of What Does Hud Have To With Reverse Mortgages?

You'll divide the overall value of real estate expenses by your income to get the front-end debt-to-income ratio for home loan approval. The back-end ratio: The back-end ratio considers your housing costs in addition to all of your other debt commitments. To compute this, build up all of your financial commitments, including your housing costs, loan payments, car payments, credit card debts, and other impressive loans.